The Case to Avoid Bonds and Bond Funds

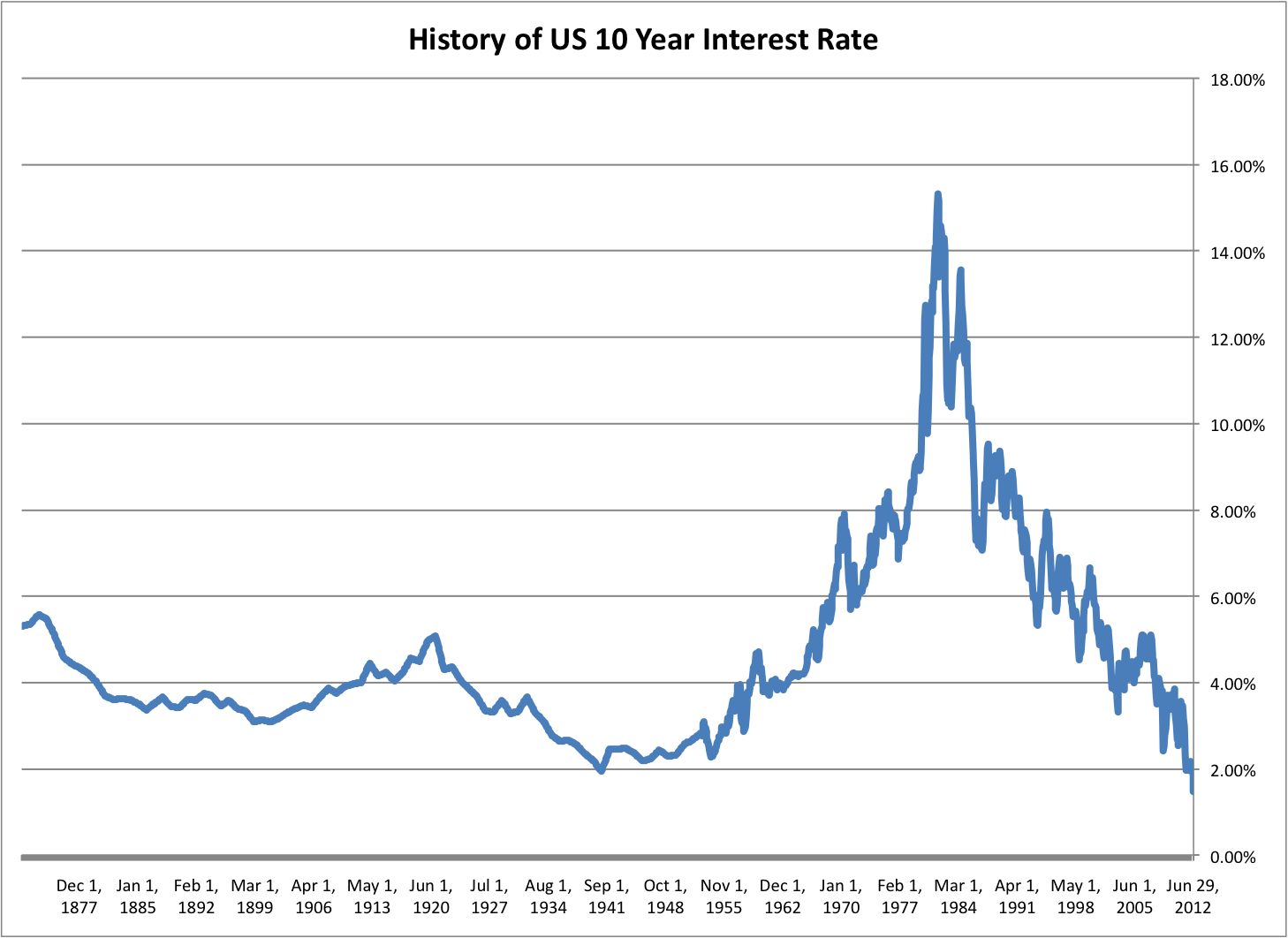

You should only have to look at the two charts above. For Canadians, our Bonds pretty much follow U.S. However we are going to go a lot deeper and I will dispel a Myth you are being told to put your IRAs, RRSPs etc. into a Bond Fund.

Bonds have historically been regarded as a safer and carry much less risk than other investments such as stocks, commodities and real estate. They offer a yield and have always been big holdings in Pension Funds. Your fund adviser (sales person) will always gleam about the safety of a Bond Fund.

However in this day and age nothing could be further from the truth. The zero interest rate and QE monetary policy around the world has meant yields on Bonds have fallen to historically low levels. It has helped fuel a 35 year bull market in Bonds, but it is not rocket science to realize there is not much room on the downside for rates to fall but the sky is the limit to the upside.

You have to realize the most important factor for returns on Bonds and Bond Funds is the price of the Bonds especially as the yield (interest rate paid) has become less and less. Bond prices rise as interest rates fall and prices fall when rates rise. A couple videos on the left explain this.

When I looked for videos on Bonds I noticed they were not very popular and I think that might be because the majority are being led down the garden path and believe there is nothing to worry about.

Ironically with the extreme high debt levels around the world, at the Country level as well as State, Municipality and Corporate levels - the risk level has gone much higher at a time when investors are paid less to take that risk.

I want to keep this section on Bonds a simple as possible because the majority of Investors have been sold a false story – being if you invest in a short term Bond Fund it will not be effected much by rising interest rates. This is simply not true and you will lose a lot of money – please see an example near the bottom

Practically on a monthly basis there is news of Countries (Greece, Puerto Rico), States, Cities (Detroit) and Corporations running into debt problems and bankruptcy. Their interest rates soar on their and Bonds the price of the Bonds plummet.

You can even find a map plot now of US Municipalities filing for Bankruptcy since 2010

While Cities and States can't print money to save themselves, Countries can but without consequence

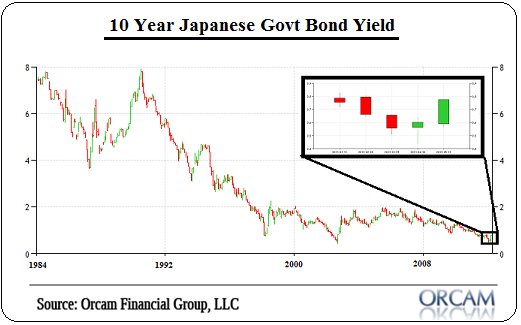

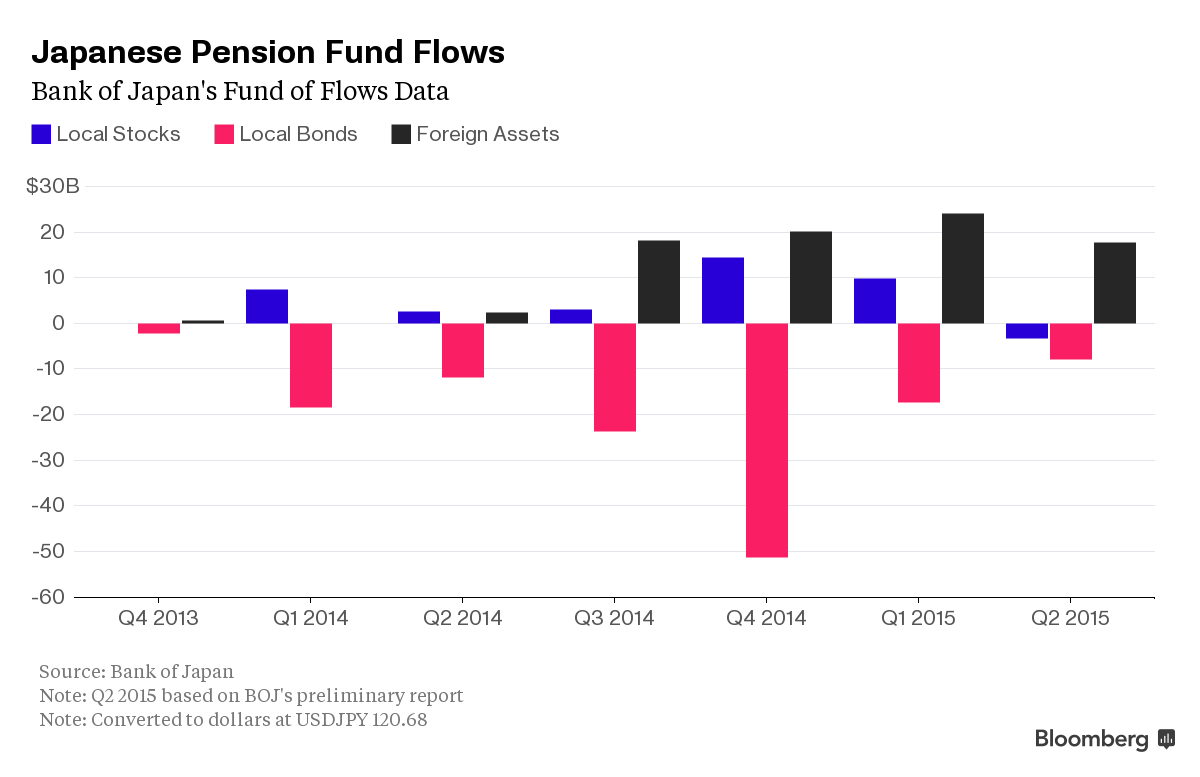

A case in point how this has worked is Japan. I am sure you have seen in the press about Japan's aggressive monetary easing and money printing to try and spur economic growth. However, that is not what has really happened. In fact the Japanese Pension funds with large Bond holdings were no longer willing to take the risk and claimed they could not afford to take the hit when rates increased.

The market would not be able to handle their massive selling so the solution was for the Bank of Japan with printed money out of thin air with keyboard stokes to buy their own Bonds while the Pension Funds sold.

Japanese Pension Funds sell record amount of Bonds

In September Japanese Government Pension Investment Fund, the world’s biggest pension fund with $1.2 trillion of investments, released its own data last month showing it has neared the end of an unprecedented shift to stocks from bonds.

You can find in lots of main stream press about Japan's economic woes. Private consumption dropped 0.8% in the last quarter, and GDP dropped 0.4%. The economy shrank in six of the past 12 quarters. And you will here that Abenomics (named after Japan PM) has not worked out for the economy.

But as I mentioned above - Abenomics was never about the economy. It is about preventing a Bond market crash and boosting the stock market and stocks have more than doubled! That’s where the real impact of Abenomics has been. It is no different in America. If you follow my commentary/analysis about the Fed, they are more concerned about interest rate hikes effecting the stock market than the economy.

Remember the Fed are Bankers and Bankers have more vested in the stock market than anyone else. I don't have to tell you the record amounts the Banks are making with their Trading/investing, ETFs and Funds.

Now lets look at examples of what you will lose with Bonds when interest rates rise

An extreme case is when a Country or any entity that issues Bonds runs into financial problems. The chart left & above is what happened in Greece with their Bonds

You no longer have to take financial course to learn how to calculate Bond prices and yields, there is a handy Bond calculator on line

In 2010 when Greek Bonds started to creep higher on debt concerns, they were yielding around 11%. Once fears took hold about default – yields soared to 40%, but lets be nice and say 30%. Below is what happened to the price of 3, 10 and 20 year Bonds assuming a $1,000 face or issue price of that Bond

11% 30% Loss

3 year $1,000 $655 -345 -34.5%

10 year $1,000 $413 -587 -58.7%

20 year $1,000 $370 -630 -63%

I have some pretty scary videos about where Japan and the U.S. is headed with their enormous debt and it will eventually be a Greece situation.

However, we don't need to be worried about a dooms day scenario. You will take big losses if interest rates only rise back to normal levels before QE and that would be the Fed increasing rates back to 3% to 4% from the current about 0% level.

So lets look at just a 3.5% rise in rates. In the past year the 10 year treasury has been yielding 1.7% to 2.5% and recently around 2.2% so we will use that level and look at the effect on a $1,000 face value Bond if rates moved up 3.5% to 5.7%

2.2% 5.7% Loss

3 year $1,000 $945 -55 -5.5%

10 year $1,000 $739 -261 -26.1%

20 year $1,000 $589 - 411 - 41%

I am just using Vanguard Bond Funds as examples, and am not suggeting buying or selling

For example the Vanguard Short Term (1 to 3.5 yr bonds) Bond Fund VFSTX has returned 1.3% to 1.5% annually over the last 3 years and with a Bond bull market 3.6% the last 10 years

The Vanguard Long Term (over 10 yr maturities) Bond Fund VBLTX is -2.5% YTD and currently 1 to 3 year annual returns between 2.0% and 2.9% and in a Bond Bull market 6.6% annually the last 10 years

But from this example with a little upward rate pressure this year the longer term fund is -2.5% this year while the short term is still positive, this was early Nov 2015, the quotes may be different if you click the links now?

The only sure way you don't lose money on a short term bond is to buy the bond yourself. Of course I am assuming a high quality bond and the issuer does not go broke.

If you buy a 2 year Bond at $1,000 face value with a 2% yield, that face value could fluctuate and go down if rates rise. However if you hold the bond to maturity you will get your full $1,000 back plus you made the 2% interest in the meantime. It does not matter how much the bond price fluctuates between the time you buy and maturity, because at maturity you get the full $1,000 value.

Now with a Short Term Bond fund that holds 2 year Bonds it will not work that way and if interest rates rise enough you will lose money. This is because a Fund does not just hold one bond that is attached to you when you buy the Fund. The Fund is continuously buying and selling bonds. As bonds mature they buy new ones, so what you hold in a Fund will always be a mixture of all kinds of different Bonds with different maturity dates, all fluctuating in price based on interest rates and the time left to maturity.

Now granted with a short term Bond Fund you should only lose -4% or -5% if rates climb a few points, but if you keep holding that Fund and rates continue to rise every year you will keep on losing money.

My point here is - in a rising rate environment the only way not to lose money is to buy the actual Bond and hold to maturity.

If you are concerned rates will rise you either buy a Bond yourself or just park $$ in 30 or 90 day treasuries. While they may only pay 0.1% or 0.2% now, if rates increase, every 30 or 90 days you roll them over and you will get a higher interest rate. In my scenario, by the end of the year they are paying 3% to 4%

I plan on adding some Bond quotes to the left so anytime you chech here you can find current yields on various maturities and countries etc.

Also beware that with low Interest rates many Bond Funds have been loading up on riskier Bonds that pay higher interest. These Bonds could be hit harder if rates increase

More to come ............................